NVDA: We Don't Have Enough Compute

Doubling Down on Nvidia

Hello! It’s been a few weeks since my last post — since then, it feels like we have lived through an entire movie that has written itself via Truth Social posts. Each new post ends up costing the economy or providing the economy with a few trillion dollars. Wall Street truly is the greatest show on earth.

I’ll be back to posting on a regular schedule, the travel has been pretty intense with going to different events (I’ll be in LA this weekend for a meetup if you’d like to come) and with streaming twice a day, being able to actually sit and write articles has been a bit tough. I don’t use any AI outside of summarizing numbers so although it is challenging to sit and write, I really do enjoy the challenge given how much I communicate through spoken word. It’s nice to embrace a new medium and put the time and effort in.

So, what have I been doing over the past few weeks?

Well, I am doubling down on Nvidia. I have doubled my position and I feel it is simply one of the best risk/rewards in the entire stock market currently right now.

This shouldn’t be that controversial. I mean, it’s Nvidia at the end of the day, right?

Well, the market continues to discount the growth forecasts, sell every rip, and doubt Jensen on his overall AI thesis.

Nvidia’s stock price action over the past month:

I have spent many weeks this year really trying to understand the story and am flabbergasted that I am able to buy stock at these levels. I began buying NVDA during DeepSeek and it’s almost like I am getting to buy it again at these levels even though the stock has doubled because the growth has also kept up, leading the multiple to compress even though the price has increased.

Alright, let’s dive into what is going on with Nvidia…

The Numbers Are Really Good

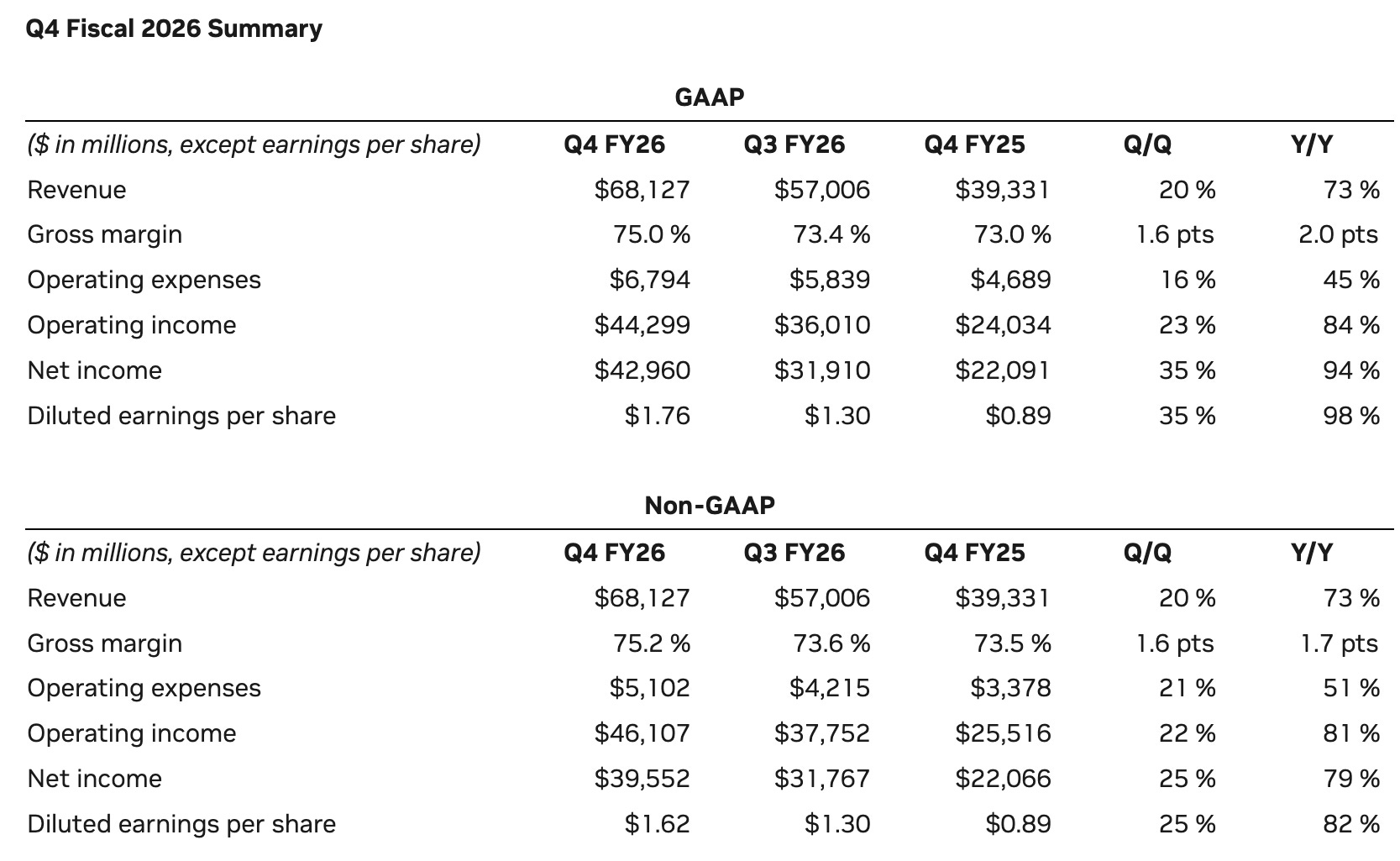

Before we get into all of the qualitative elements of how Jensen continues to speak about AI, it is really important to understand the Q4 that Nvidia just put up.

These numbers are beyond incredible. Nvidia not only beat expectations by a WIDE margin, their guide is implying an 81% YoY growth rate for Q1 which is accelerating revenues and they are likely to beat that growth rate as well since they usually beat their own guide by a few billion.

The QoQ growth as well is just exceptional…it was one of the single best quarters I have ever seen.

However, the stock briefly touched $200 and then fell. The price action since then has led to NVDA to trade at just 21 times earnings & under 16 times forward earnings.

source: Steven Fiorillo

The fact that Nvidia is still trading at these levels even after this type of a beat shows me that the market is more concerned about the war, oil prices, macroeconomic issues, and the durability of this growth. All of these are fair concerns, especially the last one, but the disagreement I have with the market on that durability is why investors are able to buy NVDA at these levels and ultimately I trust that Jensen will be right on the question of growth over the long term.

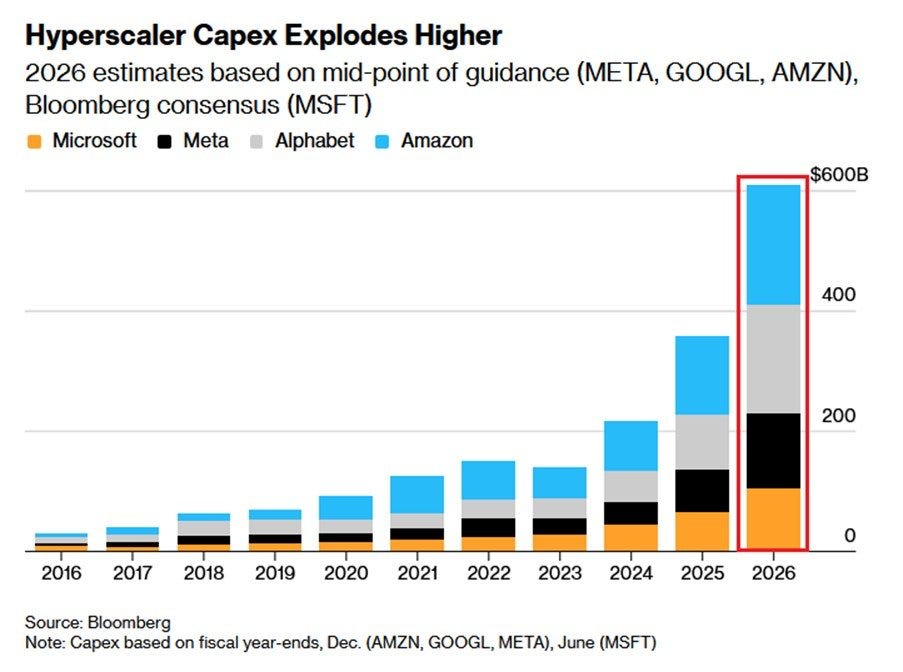

What is more important than just Nvidia’s revenue is that Big Tech CapEx has guided now that earnings are in, and boy are they ready to spend…

Now, I understand that many people doubt the cap-ex cycle to continue growing at this rate. Most people are likely correct about capex inevitably slowing down at some point. The Big Tech names are taking all of their FCF and throwing into capex, many of them raising debt with bond sales or even going negative on their FCF to fund their capex. Up until the past few weeks, even I was skeptical that this capex cycle could continue in the way that it is.

However, this is where I think the market might not be fully factoring in the value of AI. Not only are all the Mag 7 in a prisoner’s dillema of having to outspend each other in order to secure enough compute capacity to deliver on the promises to their own customers, the broader point that Jensen has been trying to make is that these companies are seeing their OWN revenues go up as a result of having more compute.

This is where you have to draw a line in the sand and ask yourself if you believe in what is going on across the broader economy: will META, AMZN, GOOGL, and MSFT continue to see the growth in their businesses which will allow them to justify the capex spend they are currently engaging in?

META guided for 33% topline revenue growth as a $1.5T company. All of this is from their ads being so good because of AI that they can keep growing.

GOOGL grew cloud revenues 48% last quarter. This is due to increased AI demand.

AMZN grew AWS by 24% and guided to $600B of revenue for AWS by 2035. The AWS CEO stated that if they had more compute, they’d be able to grow faster.

When you look at these examples, along with many more companies outside of the Mag 7 that are either spending on datacenters or paying the hyperscalers to access their datacenters, it becomes more obvious that capex is not going to slow and the mindset shifts to the world not having ENOUGH compute rather than assuming compute has a cap on it. There is, quite frankly, zero cap to the potential of what this compute can bring to the world…which is why Jensen is upset.

Jensen Is Upset

Jensen recently spoke at the Morgan Stanley tech conference and the final question was about the stock price being flat for the better part of 8 months. He gave a long response but it is well worth the read and lays out the plans for how he is thinking of the future growth prospects for Nvidia:

“I care about shareholders, I care about our employees. I care about all of you. And you might be referring to—we just had the best earnings in the history of earnings. Is that what you were saying? I mean, somebody actually told me that this might be the single best print in the history of humanity. And I said it must be only, you know, recorded humanity. I’m sure somebody had better returns.

But anyways, we had a very good quarter. Listen, you can’t hold the stock back. You can’t hold it back. And the reason for that is very simple. Compute equals revenues for companies. In the future, every single company will need compute for revenues. I’ll just make that prediction for now. Every single company will need compute for revenues.

And the reason for that is because compute translates to intelligence, which translates to your digital workforce, which translates to your revenues. I’m certain compute equals revenues. I’m certain also that compute equals GDP. Therefore every country will have it because not one country in the future will say, guess what, we’re going to opt out on our own intelligence. We’ve got—I don’t know what we got—but we don’t need intelligence. That’s the one thing we don’t need.

And so if you need intelligence, you’re going to need digital. You need AI, you’re going to need compute. And so compute equals GDP. I know that for certain. I also know that we’re at the beginning of this journey. And I see crystal clearly exactly how it’s going to get funded.

We know for a fact that all the CSPs took all of their CapEx and they converted it to generative, agentic systems, AI systems, because it helps search, because it helps shopping, because it helps ads, because it helps social, because it helps literally every single internet service in the world has been reinvented into generative AI.

So they could take 100%—the entire internet industry could take 100% of their CapEx and make it AI because it’s better, we’ve proven it to be better. Meta has proven it to be better. Google has proven it to be better. AWS has proven it to be better.

And so you can now take your CapEx and convert to this. Number two, I just said the entire software industry will be token driven, the entire software industry. You pick your favorite software company, and I can show you exactly how they’re going to be token driven. And that token—you take your favorite software company—their token will be either produced by themselves, which needs compute, or it could be resold, and that needs compute.

And so what that says for the first time is the entire IT industry will have to be fueled by compute. That’s exactly where all this is going to come from—trillions of dollars of it. And we’re at the beginning of that. So that’s my prediction.”

I thought this syllogism by Jensen was incredibly important to understand when it comes to Nvidia.

Essentially, he’s saying:

More Compute —> More Tokens —> More Revenue

If you believe that you can monetize tokens, then tokens require more compute. If companies want more intelligence to transform their businesses (tokens) they will then need to spend on more compute which is what Nvidia provides. Even if the cost of tokens fall, the demand exceeds the cost decline by orders of magnitude which is what leads to sustained, durable revenues for Nvidia on their datacenter business.

What is the logic behind more compute leads to more revenue? Well, we’ve seen it in a few examples:

ChatGPT can sell more subscriptions with more compute

META can sell better ads with more compute

GOOGL, MSFT, AMZN can sell more cloud with more compute

TSLA can sell more FSD (and eventually robots) with more compute

Software companies can sell more agents with more compute

The agentic part is what I want to focus on. I was just at NVDA’s GTC event and the core announcement they had was around NemoClaw, which is their version of bringing OpenClaw to the enterprise. I asked Jensen a question at GTC that you can watch here and interviewed two Nvidia executives that you can watch here.

OpenCLAW is an open-source framework designed to help developers build and deploy large-scale AI agents and workflows. It focuses on orchestrating models, tools, and data pipelines so AI systems can perform complex, multi-step tasks. The goal is to make agent-based AI systems more modular, reproducible, and easier to scale across real-world applications

NeMo-CLAW is an extension within NVIDIA’s NeMo ecosystem that applies these agentic concepts to enterprise AI. It integrates large language models with tools, retrieval systems, and structured workflows to enable production-grade AI agents. The platform is built to power use cases like digital employees, automation, and domain-specific AI systems using NVIDIA’s infrastructure and software stack.

While everyone is arguing that software is dead, which I will have on article soon on, Jensen’s argument is that these agentic workflows are going to be one of the most important part of the enterprise and help companies like CRM, ADBE, NOW, etc. continue to sell more software and grow. Agents allow more things to get done quicker, but they also burn massive amounts of tokens. Jensen went as far as to say that OpenClaw became the iPhone moment for agents, and if he’s right, we will continue to see more and more spend on compute.

Anthropic and OpenAI’s growth is undeniable

Anthropic was doing $14B ARR in January. They are now doing $20B in March because they added $6B in February.

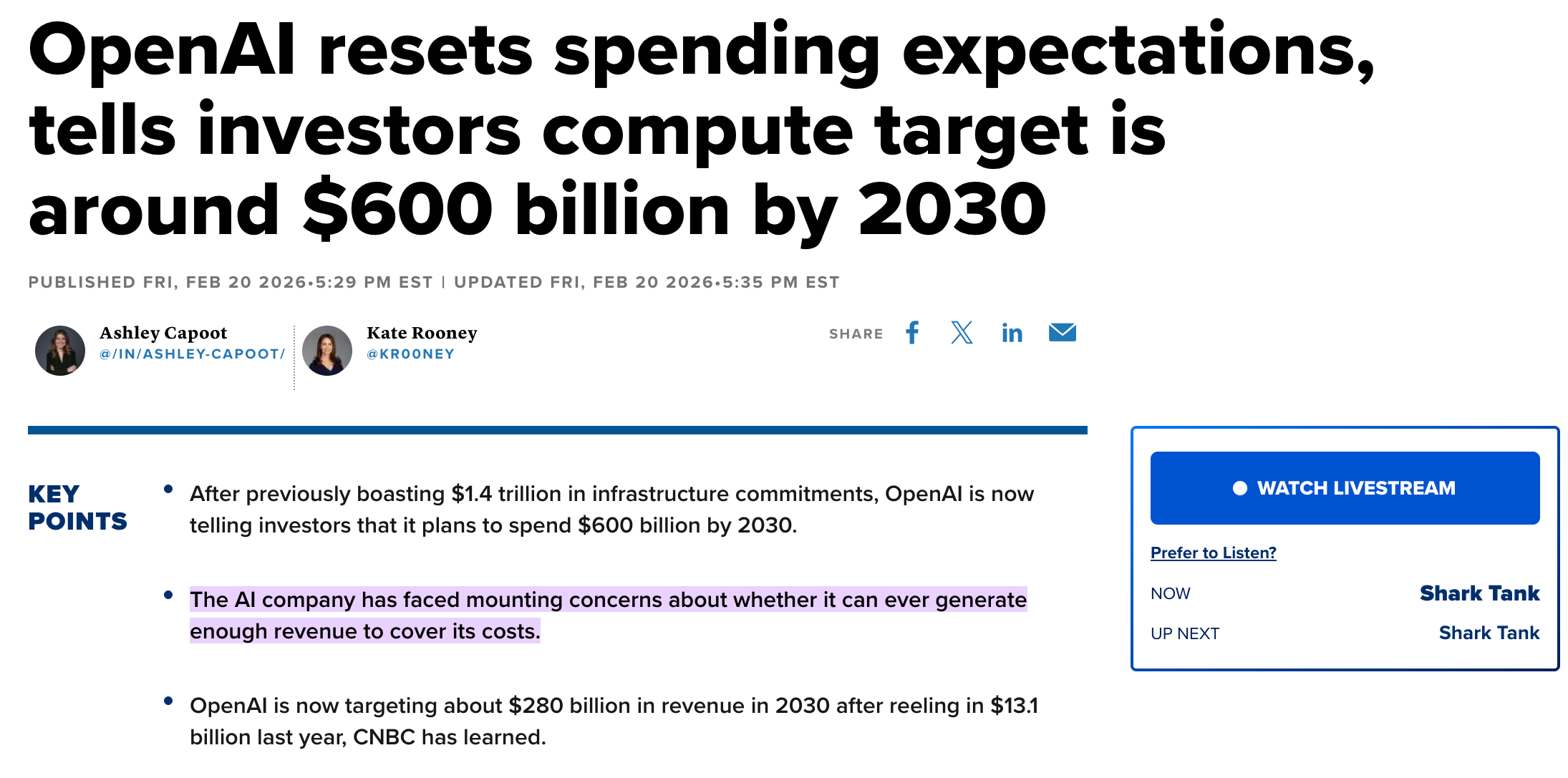

OpenAI is now doing $25B ARR and expecting to bring in $280B by 2030.

The type of growth we are seeing from the foundation model companies is absolutely unprecedented and Jensen knows this, which is why NVDA just invested $30B into OpenAI and $10B into Anthropic. He expects this to be the last funding round before both companies go public.

Now, these are two really important companies when it comes to understanding Nvidia. Why? Well, they are the ones that are going be distributing most of the usecases that allow compute to continue to be sold and resold.

Anthropic has been on fire over the past two months. They are actually seen as the reason for the software selloff because they continue to introduce new products that enterprises are adopting at a rapid scale, ClaudeCode and ClaudeCoWork being the biggest.

OpenAI has 910M weekly active users and Codex is growing 25% per week. Coding is the first major usecase that these companies have discovered for the enterprise but there are many, many more coming. Palantir, which creates software to orchestrate the LLMs inside of an enterprise, just grew revenues at 70%.

What happens when 4B people per day are using these models? What happens when 5M businesses per day are using these models? The growth of these foundation model companies is likely going to be more than we can possibly imagine. I recently used Claude to vibecode my own website and it took one hour. I just spoke english and the product was done. This is not reversing. This trend is only going to be more exciting, more influential, will make everyone more productive — but it is going to require MORE compute. We simply don’t have enough of it which is why the cycle will not only continue but Nvidia will be at the center of the cycle.

To conclude, I want to leave a quote that Jensen gave just recently on the Lex Fridman podcast, discussing on the potential revenue growth for Nvidia, which really gives you a look into his state of mind on how big this company can become:

“Is it possible for NVIDIA to be a, you know, $3 trillion revenues company in the near future? The answer is of course yes. And the reason for that is because it’s not limited by any physical limits. There’s nothing that I see that says, you know, gosh, $3 trillion is not possible. And as it turns out, NVIDIA’s supply chain is—the burden is shared by 200 companies.

And the fact that we scale out on the backs with the partnership of this ecosystem, the question is do we have the energy to do so? And surely we will have the energy to do so. And so all of these things combined, that number is just a number, you know? And I still remember, NVIDIA was a—NVIDIA was a—the first time we crossed a billion dollars, I was reminded of a CEO who told me, “You know, Jensen, it’s theoretically impossible for a fabless semiconductor company to exceed a billion dollars.”

And I won’t bore you with why, but in the end, of course it’s illogical and there’s a lot of evidence we’re not. And then somebody told me, “You know, Jensen, you’ll never be more than $25 billion because of some other company.” Somebody told me that, “You’ll never be, you know, because…” And so those aren’t first principled thinking.

And the simple way to think about that is what is it that we make and how large is the opportunity that we can create? Now, NVIDIA is not in the market share business. Almost everything that I just talked about doesn’t exist. That’s the part that’s hard.”

Thank you for taking the time to read and let me know any ideas you’d like to see me write about!

More consistent posts, please!

Yep. Basically. Geopolitics is noise. This is what will matter in 20 years.