Dumpster Diving: 10 Stocks Getting Crushed YTD That May Deserve A Second Look

One man's trash is another man's treasure

Alright, it has been a massive bull run…but not for everybody.

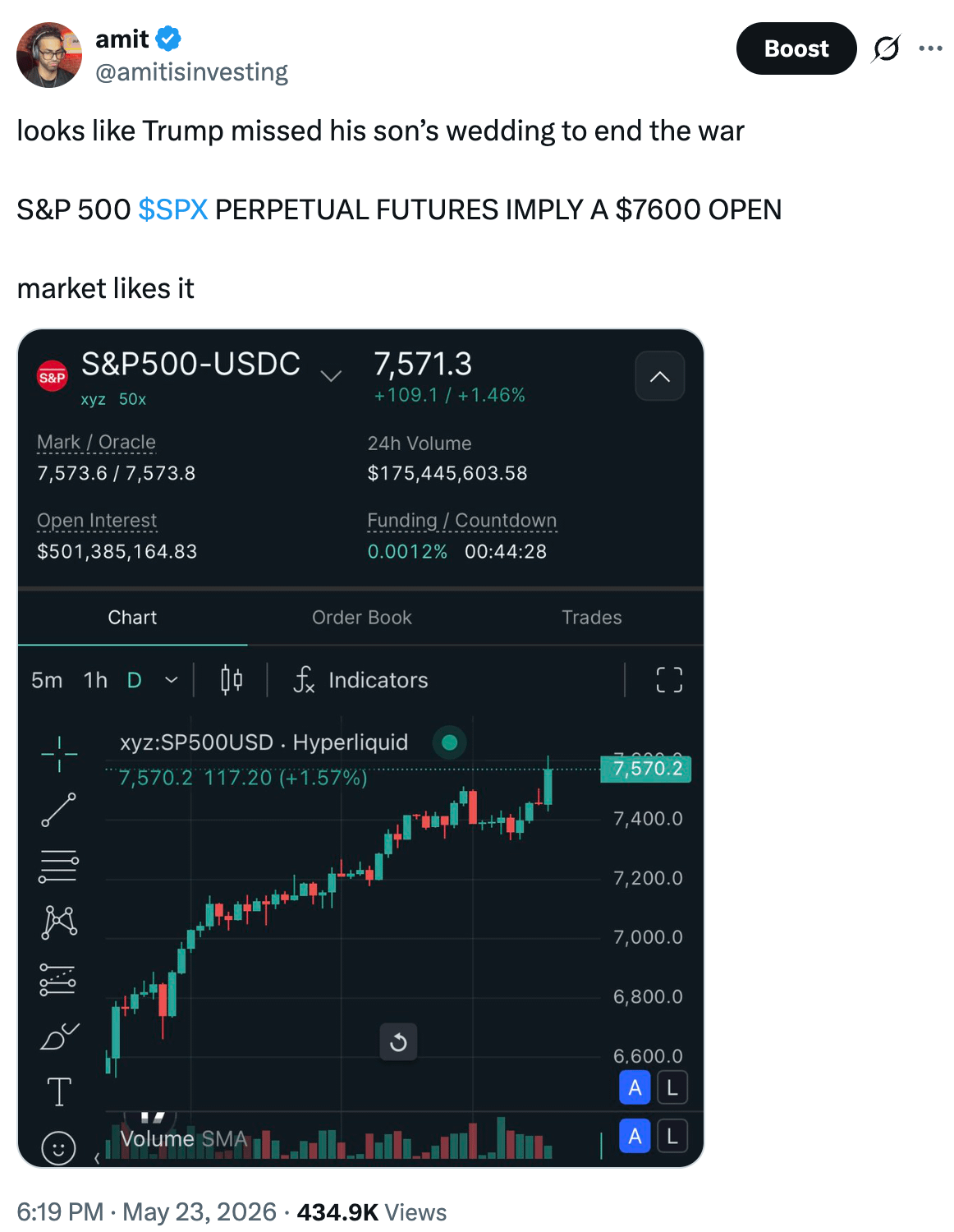

As of today, May 25th, it looks like we might start seriously seeing some progress on the Iran War. Multiple news sources have indicated that the war is coming to an end, a ceasefire will be extended, the framework for a deal is being put in place, and maybe…just maybe…oil can come down so that CPI and PPI aren’t as aggressive and we could have a chance for lowering rates this year.

S&P 500 Futures are implying an open close to $7600 after the news was announced yesterday that the war may be coming to an end:

Having said that, not every stock is up year to date, in fact many of them will be down even if the S&P hits new all time highs above $7600. Why? Well, the market has had a variety of challenging issues with stocks in different sectors. I am not going to make the case that the following stocks are buys. I am also not going to make the case that the market will rotate into these stocks if we hit a local top (in fact we will probably see these names get crushed with the broader market) but I am going to highlight 10 names that are exceptional businesses, and if we can ignore the stock price action and focus on the core business, one could come to the conclusion that some of these names are not in the right theme right now (ai, robotics, etc.) but are compounders that likely can produce meaningful earnings growth over time.

Two things before we get into it — First, I just launched a brand new retail bloomberg-like news terminal. It’s 100% free. If you want to support by paying $5/month you can, but I encourage people to join it and see if it changes how they get the news daily. You can check it out here.

Second, the humanoid robotics theme is becoming pretty exciting. I am an early investor in Figure ($2.6B entry) and Apptronik ($250M entry) so I feel that I understand the space relatively well…I’ll be working on some analysis around the sector, best way to get exposure, how realistic the scaling process is for these bots to become mainstream, and what elements of the supply chain do we need to look at in order for the sector to get more attention. Excited to work on this research.

Alright, 10 names that are down bad YTD but deserve a second look…

SOFI

SoFi is one of the cleaner setups because the business is no longer just a high-growth fintech story, it is now consistently profitable. I recently had the CEO on for a podcast, and he blamed the stock price performance primarily on rate cuts and the market’s lack of being excited for any company that has exposure to a changing rate environment, which is why banks have been pretty bad this year in terms of performance along with all fintechs. SoFi looks attractive because the stock has been punished year to date, but the company’s financial profile has materially improved. In Q1 2026, SoFi reported adjusted net revenue of $1.1 billion, up 41% year over year, with GAAP net income of $166.7 million, up 134% year over year. Adjusted EBITDA was $340 million, up 62% year over year, and the company posted an impressive Rule of 40 score of 72%, which shows the combination of growth and profitability is becoming much stronger.

The operating metrics are also moving in the right direction. SoFi reached 14.7 million members, up 35% year over year, and 22.2 million products, up 39% year over year. That matters because SoFi is not just adding users — it is expanding product adoption across its customer base. The more checking accounts, loans, investing accounts, credit products, and financial services a member uses, the more valuable and sticky that customer becomes.

The bull case is that the market is still valuing SoFi like a risky, rate-sensitive lender, when the company is increasingly becoming a profitable digital financial platform. Management also guided for Q2 adjusted net revenue growth of approximately 30%, with an adjusted EBITDA margin around 30% and adjusted net income margin around 12%–13%. If SoFi keeps growing members, expanding products, and improving profitability, the current drawdown could look like a reset in a company that is finally entering its earnings-compounding phase.

META

Meta is not down as much YTD, but it’s lack of performance given it’s growth and it’s fall from the $750s is what is concerning to investors. Meta is one of the clearest examples of a stock being punished more for investor fears than business deterioration. In Q1 2026, Meta generated $56.3 billion in revenue, up 33% year over year, while income from operations reached $22.9 billion, up 30% year over year. Operating margin remained extremely strong at 41%, and net income rose 61% year over year to $26.8 billion, with diluted EPS up 62% to $10.44.

The main concern around Meta is not the core business, it is the spending cycle. Investors are worried about massive AI capex, infrastructure buildout, and whether Reality Labs and AI investments will earn acceptable returns. But the core advertising machine is still one of the best businesses in the world. Facebook, Instagram, WhatsApp, Threads, Reels, and Meta AI give the company unmatched distribution across billions of users, and the company is still producing elite margins while investing aggressively.

The bull case is that AI strengthens Meta instead of hurting it. Better AI can improve ad targeting, content recommendations, creator tools, messaging commerce, business automation, and advertiser ROI. If Meta’s AI investment leads to better engagement and better monetization across its family of apps, then today’s capex concerns may end up looking like the cost of building the next major growth layer. When a company growing revenue 33% with a 41% operating margin sells off, it deserves attention.

MSFT

Microsoft remains one of the highest-quality companies in the market, and any meaningful year-to-date pullback gives investors a chance to buy an elite compounder at a less stretched valuation. In fiscal Q3 2026, Microsoft reported $82.9 billion in revenue, up 18% year over year, while operating income increased 20%. EPS was $4.27, up 21% after adjusting for the impact from its OpenAI investment.

The cloud numbers are the center of the bull case. Microsoft Cloud revenue reached $54.5 billion, up 29% year over year, and commercial remaining performance obligation increased 99% to $627 billion. That backlog number is massive because it shows future contracted demand across Microsoft’s enterprise stack. Productivity and Business Processes revenue was $35.0 billion, up 17%, with Microsoft 365 Commercial cloud revenue up 19%.

The reason Microsoft is attractive on weakness is that it sits directly in the path of enterprise AI adoption. Azure gives it infrastructure exposure, Microsoft 365 gives it workflow distribution, GitHub gives it developer mindshare, and Copilot gives it a way to monetize AI across knowledge workers. Investors may worry about AI capex and near-term margin pressure, but Microsoft is still one of the most important toll roads in cloud, productivity software, security, and enterprise AI.

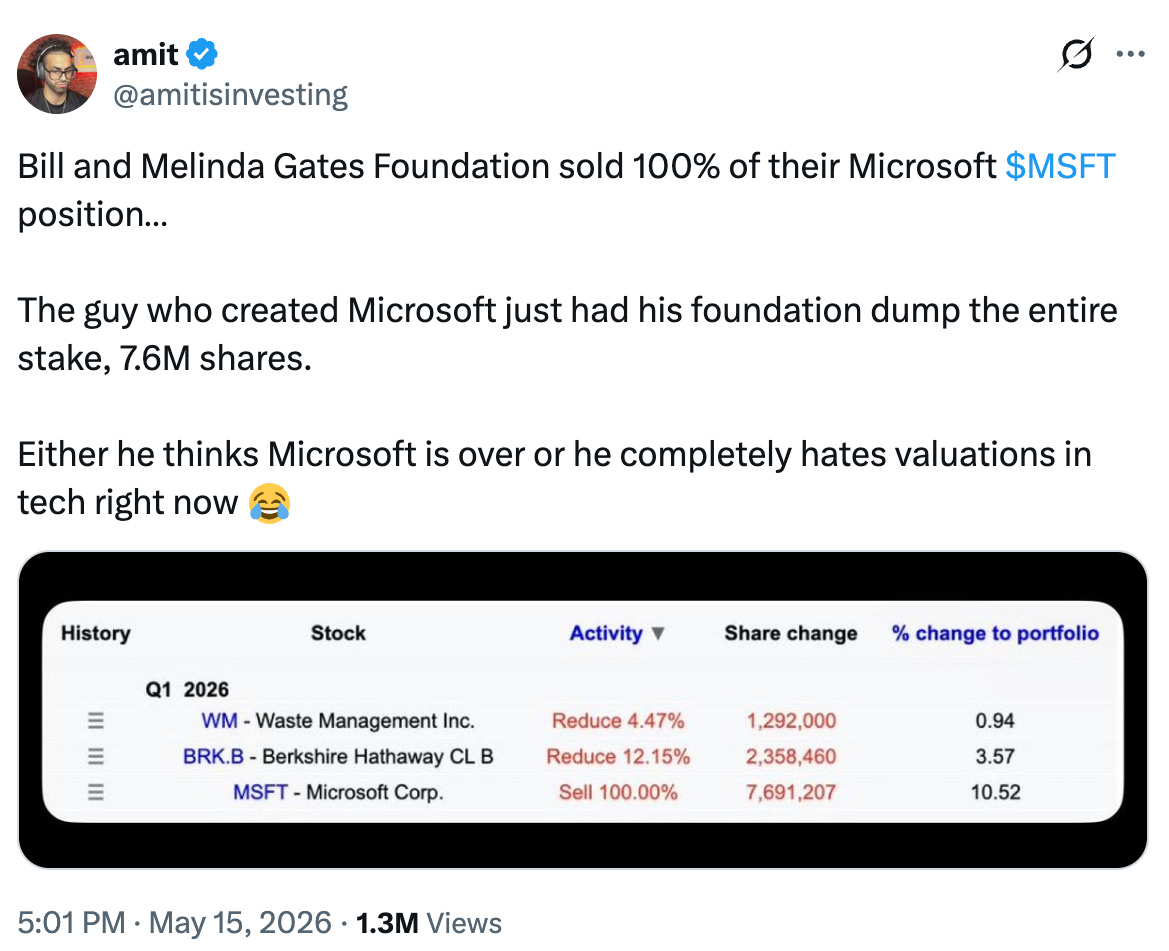

Also…I mean…it’s MICROSOFT! It is worth noting that the Gate Foundation sold their entire stake…a weird time for MSFT, but it is indeed one of the most important companies on Earth.

GRAB

Grab is compelling because the company is moving from a high-growth, subsidy-heavy app business into a platform with real operating leverage. In Q1 2026, Grab reported revenue growth of 24% year over year, with adjusted EBITDA up 46% year over year to a record $154 million. For a company that investors once doubted could ever become meaningfully profitable, that is a major improvement.

The company also reaffirmed full-year 2026 guidance for revenue of $4.04 billion to $4.10 billion and adjusted EBITDA of $700 million to $720 million. That implies Grab is not just growing revenue, it is converting more of that revenue into profit. The platform is benefiting from scale across mobility, delivery, financial services, advertising, and merchant tools, which gives Grab multiple monetization levers across Southeast Asia.

The bull case is that Grab becomes the dominant super-app infrastructure layer for Southeast Asia. Mobility and delivery bring users into the ecosystem, fintech and payments increase monetization, and advertising can become a high-margin layer on top of merchant activity. If Grab keeps growing revenue in the 20%+ range while expanding EBITDA, the market could eventually value it less like a risky emerging-market app and more like a durable regional platform. The main reason I think it is down is because of the oil crisis for Asia (even though the company is managing it very well) so hoping that lower oil can continue to be a tailwind for them. At some point, 50% of the company’s market cap in cash and the growth should get respect from the market.

SE

Sea Limited is attractive because the company has already gone through a brutal valuation reset, but the fundamentals are improving across the core businesses. In Q1 2026, Sea reported revenue of roughly $7.1 billion, up 46.6% year over year, with net income of $438.2 million and adjusted EBITDA of approximately $1.0 billion. Operating income grew nearly 30% year over year to about $593 million.

The strength is broad-based. Shopee remains one of the dominant e-commerce platforms in Southeast Asia, and e-commerce continues to drive the majority of company revenue. Monee, the financial services business, generated $1.2 billion in revenue, up 57.8% year over year, while adjusted EBITDA in that segment reached $275.2 million, up 14%. Consumer and SME loans principal outstanding reached $9.9 billion, up 71.3% year over year, showing how quickly the fintech layer is scaling.

The bull case is that Sea is no longer just a pandemic growth stock or a one-product gaming story. Shopee gives it e-commerce scale, Garena gives it gaming upside, and Monee gives it a fast-growing fintech engine attached to the commerce ecosystem. The risk is that growth investments and credit losses can pressure margins, but if Sea keeps growing near 40%–50% while staying profitable, the stock could re-rate meaningfully from depressed levels.

APP

AppLovin is one of the strongest fundamental stories in the group because the profitability is almost absurd for a company still growing this quickly. In Q1 2026, AppLovin generated $1.84 billion in revenue, up 59% year over year. Net income rose 109% to $1.21 billion, adjusted EBITDA reached $1.56 billion, and the adjusted EBITDA margin was roughly 85%.

The free cash flow profile is the biggest reason the stock remains interesting despite volatility. AppLovin generated about $1.3 billion of operating cash flow and $1.3 billion of free cash flow in Q1 alone. The company also repurchased and withheld 2.2 million shares for a total cost of about $1.0 billion, showing that management is using the cash machine aggressively while the stock is under pressure.

The bull case is that AppLovin is becoming an AI-powered advertising infrastructure company, not just a mobile gaming ad platform. If its models continue to help advertisers acquire users more efficiently, more ad dollars can move through its software platform. The valuation risk is real because expectations are high, but when a company is growing revenue nearly 60%, producing an 85% EBITDA margin, and generating over $1 billion in quarterly free cash flow, a pullback can create a very attractive risk/reward. The CEO has also recently started to do many, many more podcasts after years of being in the dark, indicating that the company is more ready to showcase their story and get the public to understand why they should trade at a higher multiple.

RDDT

Reddit is attractive because the market may still be underestimating how powerful and under-monetized the platform is. In Q1 2026, Reddit reported revenue of $663 million, up 69% year over year. Daily Active Uniques increased 17% year over year to 126.8 million, while net income reached $204 million, equal to 31% of revenue. I did a deepdive on this back at $230, I was not interested because of valuation…but valuation has gotten much better and one could argue it is significantly cheaper now that growth is up.

The profitability inflection is what makes Reddit more interesting now than it was at IPO. Adjusted EBITDA was $266 million, up 131% year over year, representing a 40% adjusted EBITDA margin. Operating cash flow was $312 million, equal to 47% of revenue, and free cash flow was roughly $311 million. ARPU rose 44% to $5.23, showing that Reddit is not just growing users, it is monetizing them much better.

The bull case is that Reddit owns one of the most valuable human-intent datasets on the internet. People go to Reddit to discuss products, stocks, technology, cities, games, health issues, hobbies, purchases, and niche communities. That content is valuable to advertisers, search engines, and AI companies. If Reddit keeps improving ads, search monetization, international ARPU, and data licensing, the company can become a much larger, high-margin internet platform.

NOW

ServiceNow is a high-quality software name that has been punished with the broader SaaS selloff, but the business itself remains extremely strong. In Q1 2026, ServiceNow reported total revenue of $3.77 billion, up roughly 22% year over year, with subscription revenue of $3.67 billion. Remaining performance obligation reached $27.7 billion, while current RPO was $12.64 billion, up about 21% year over year in constant currency.

The margin and cash flow profile are still elite. ServiceNow generated $1.67 billion in free cash flow in Q1, representing a 44% free cash flow margin. Non-GAAP operating income was approximately $1.2 billion, with a 32% non-GAAP operating margin. For full-year 2026, the company guided to subscription revenue of roughly $15.74 billion to $15.78 billion, with around 21% constant-currency growth, a 31.5% non-GAAP operating margin, and a 35% free cash flow margin.

The bull case is that ServiceNow may be one of the software companies that benefits from AI instead of getting disrupted by it. AI agents still need workflow routing, permissions, approvals, audit trails, governance, and integration into enterprise system, and that is exactly where ServiceNow lives. If the market moves from “AI kills SaaS” to “AI increases demand for workflow automation,” ServiceNow could be one of the first high-quality software names to re-rate. It’s hard to imagine this company gets vibe coded away. Jensen is very bullish on them as well and the CEO bought $3M worth of stock at $103 a few weeks ago.

CHTR

Charter Communications is a more contrarian buy than the other names because the stock is being punished for real concerns: broadband subscriber losses, cord-cutting, higher capex, and competition from fiber and fixed wireless. In Q1 2026, revenue declined 1.0% year over year to $13.6 billion, adjusted EBITDA fell 2.2% to $5.6 billion, and net income attributable to Charter shareholders was about $1.2 billion. The headline numbers were not great, which is exactly why the stock has been hit so hard.

The bull case is that even with weak growth, Charter is still an enormous cash-generating broadband business. The company produced $4.3 billion of operating cash flow and $1.4 billion of free cash flow in Q1, despite elevated capital spending of $2.9 billion tied to network evolution and upgrades. Mobile remains one of the bright spots: mobile service revenue grew 15.1% year over year to $1.1 billion, helped by mobile line growth and pricing. Commercial revenue also increased 1.0% to $1.8 billion, showing the business is not entirely dependent on legacy video.

The reason Charter can work from depressed levels is that the market may be pricing it like broadband is structurally broken, when the more likely outcome is slower growth, higher competition, and still-significant cash flow. The Cox acquisition could also make Charter the largest U.S. cable and broadband provider, with roughly 38 million subscribers and expected cost synergies of around $500 million within three years. The risks are real because internet subscribers fell by about 120,000 in Q1, video revenue declined 9.2%, and debt remains high (although at a relatively decent rate) but if broadband losses stabilize, mobile keeps scaling, capex eventually normalizes, and the Cox deal creates synergies, Charter could re-rate from a deeply pessimistic valuation.

SHOP

Shopify is a strong “buy the pullback” candidate because the stock has been hit even though the business is still growing at a premium rate. In Q1 2026, Shopify reported $3.17 billion in revenue, up 34% year over year, while gross merchandise volume cleared $100.7 billion, up 35% year over year. Gross profit reached $1.55 billion, up 32% year over year, which shows that merchant activity, platform usage, and monetization are still compounding at scale.

The profitability profile also continues to improve. Shopify generated $382 million of operating income, up 88% year over year, and $476 million of free cash flow, up 31% year over year, with a 15% free cash flow margin. Monthly recurring revenue reached $212 million, up from $182 million a year ago, showing continued strength in subscription revenue. The GAAP net loss of $581 million was mostly driven by equity investment losses, while net income excluding equity investment impacts was $360 million, up from $226 million last year.

The bull case is that Shopify is becoming the commerce operating system for businesses around the world. It benefits from e-commerce growth, payments, logistics, B2B commerce, offline retail, international expansion, and AI tools that help merchants run stores more efficiently. Management also guided Q2 revenue growth in the high-20% range, gross profit growth in the mid-20% range, and free cash flow margin in the mid-teens. If Shopify keeps growing revenue above 25% while producing durable free cash flow, the current weakness looks more like a valuation reset than a broken story.

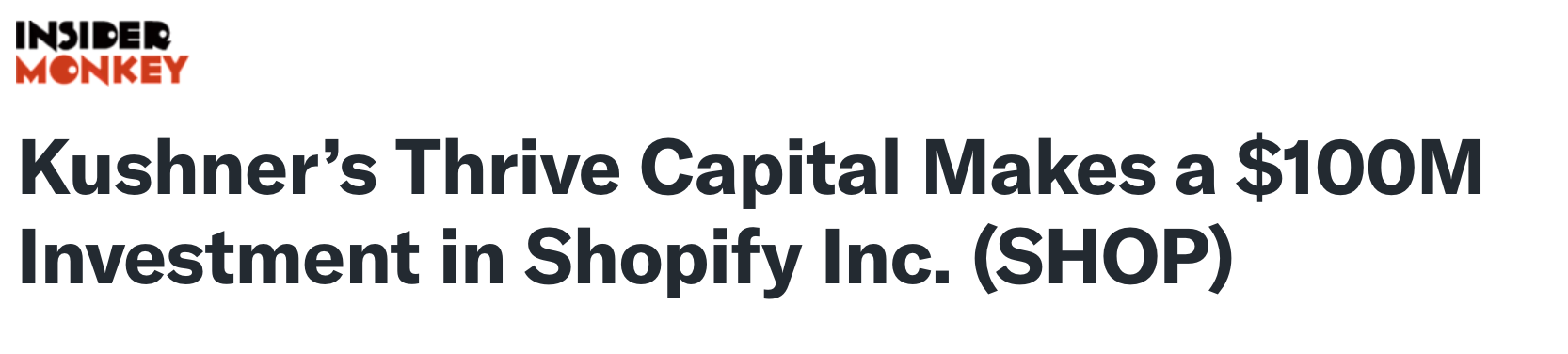

Thrive Capital is now also in as of Q1 2026, they bought the dip and likely at a price much higher than it is today since the stock has continued to go down into the low $100s and below.

I have always loved this stock, I am still trying to do deeper DD on the name, but it is one to keep an eye on since it doesn’t usually provide these types of entry points.

Let me know if there are other names you are keeping an eye on, while semis are leading the market’s rally and quite frankly may continue to, there are other opportunities that you will need to exercise delayed gratification on, but they do exist.

Thank you for taking the time to read the deep dive — truly appreciate your time and let me know your thoughts in the comments and what other companies you’d like me to dive into!

Thanks for taking time and giving such a wonderful explanation. Which of these stocks you own vs planning to own soon?

Well I'm deep into the dumpster then. lol. I have positions in NOW, SOFI, and GRAB. Long on all of them.